Let's compare savings rates.

me vs you vs everyone

I mean, the sky is falling after all, isn’t it? Tariffs, fallout, economic uncertainty, you know, generally the end of the world … yet again. It's the same old story since the beginning of time. But, since none of us own a crystal ball, why don’t we talk about battening down the hatches and saving some money for the apocalypse?

If we discuss saving money, we can’t skip the most critical piece: Savings Rates.

When you think about the typical American consumer, savings rates are probably pretty gloomy. Let’s ask ChatGPT what’s happening with the savings rates right now.

“**Americans today are saving far less out of each paycheck than they did even a couple years ago: the Bureau of Economic Analysis (BEA) puts the March 2025 personal‑saving rate at just 3.9 percent of disposable income—barely one‑tenth of its COVID‑era spike—while the typical household keeps only about $8 000 in liquid accounts, and a majority still couldn’t pay an unexpected $1 000 bill from savings. Yet averages hide large gaps: younger and lower‑income families often have negative saving, whereas high‑income households still set aside 10 percent or more. Below is a data‑driven snapshot of U.S. saving in 2024‑25.”

- AI

Yikes. That’s a recipe for disaster no matter how you look at it, financial downturn or not. At those rates, a person could never retire or weather any personal storm that might come.

Savings Rate on F.I.R.E.

It’s been a little while since I checked on my own savings rate, or trolled r/financialindependence to see what others are saying. Of course it goes without saying that the higher your savings rate, the quicker you will reach financial goals and financial independence.

Sure, some of F.I.R.E. does depend on income, but honestly, the bigger porition is probably the savings rate. Plenty of six figure folks live paycheck to paycheck, and plenty of teachers end up being millionaires.

I mean there is no end to the debates around how to calculate savings rates, what it should be, and the overall downsides and upsides to abnormally high savings rates. Seems there is opinions and numbers all over the board.

I’m not sure what all the right answers are, other than that each us should TRACK and KNOW what our savings rate is.

How I calculate savings rates.

So you can do what you want, join the arguments or whatever, but this is how I do it.

savings_rate = \

(

(income_after_taxes_and_non_retirement_deductions - expenses)

/

income_after_taxes_and_non_retirement_deductions

) * 100First, I get my income for a month after taxes and medical deductions etc. Then I jump over to EveryDollar.com and look at my budget, what were my expenses that month? Do the subtraction, get my savings number and then do the division.

What’s my currently loosey-goosey savings rate. (This probably isn’t exact, but close enough)

36%

Akk. Could be better, could be worse. On the bright side I have purposefully been spending more of late. I’ve had my years of super high savings rate of %50+, but that is not fun over the long run.

Life is short, I believe I can still have a reasonable savings rate while spending money on just being happy.

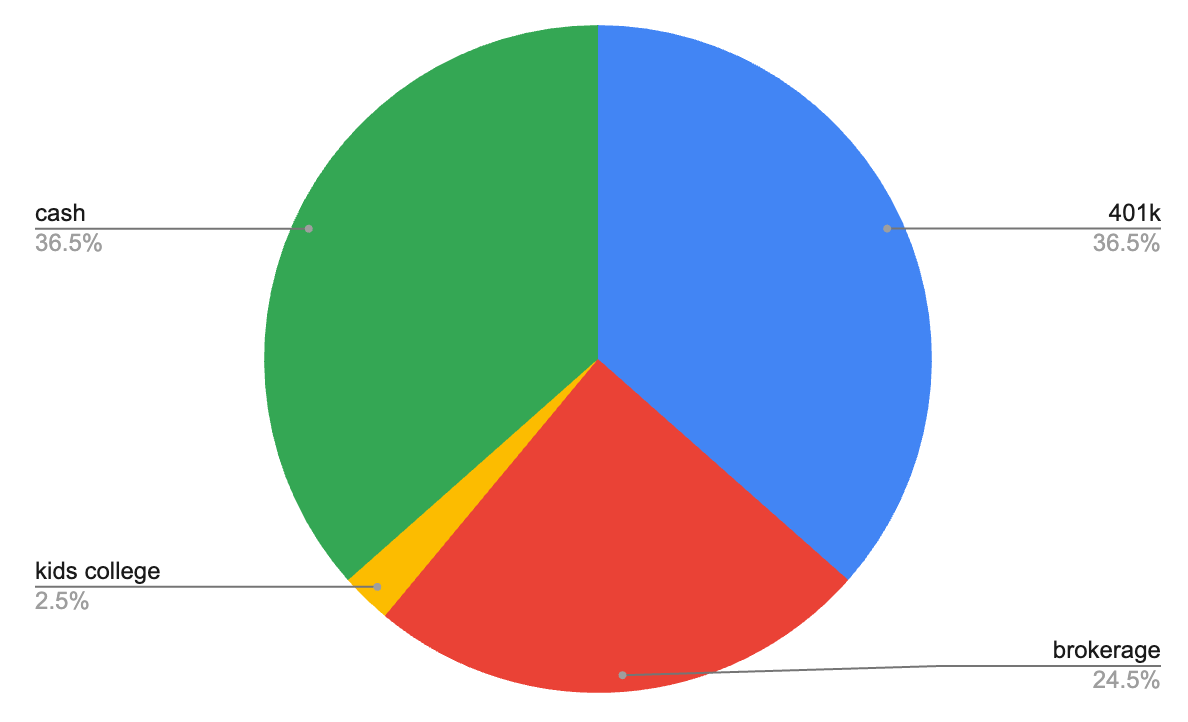

How is that savings split up, where does that money go? (so the cashflow after all expenses are paid).

What jumps out at you?

For me I think kicking up the kids college savings funds a little wouldn’t hurt. Also, probably a bit too much just sitting in cash every month, maybe redirect some of that into the brokerage account? Granted I need that cash for things like … finishing the basement, buying myself Jeeps, and the like.